Procedure for filling out an income tax return

An example of a correct income tax return in 2017, download a new current form for free in Excel. What...

An example of a correct income tax return in 2017, download a new current form for free in Excel. What's new in the declaration that you need to remember when filling it out? You can download the completed sample and form in this article.

4 times a year, organizations using the classical tax regime fill out an income tax return. From the beginning of 2017, filling out must be done using a new form approved by order MMV-7-3/572@ dated 10/19/16. You can download the profit declaration form and sample completion for 2016 in the article for free in excel format.

The new declaration form takes into account a number of changes that have been introduced since the beginning of 2015, including an increase in the rate on income in the form of dividends to 13 percent, the introduction of a trade tax in the Moscow territory and other innovations.

A number of sheets have undergone changes, new fields have been introduced, and fields that are no longer relevant have been removed. In addition, two new sheets 08 and 09 appeared in the new form.

New income tax return form 2017 form - .

Features of declaring income by an organization on the OSN:

In the new declaration form, in force since 2017, only those sheets whose contents are relevant to the taxpayer should be filled out. Mandatory are the title page, sheet 02 with the first two appendices, as well as section 1.1. When paying advances each month, section 1.2 is also completed.

In addition to those indicated, the income tax return form contains many other sheets to reflect various information. The organization must select the required sheets.

The filling procedure should be carried out as follows:

Below is a completed sample declaration for an organization paying income tax for 2016. The deadline for submitting the form is March 28, 2017 inclusive.

With regard to income tax, the deadlines for filing returns in 2017 are determined by the Tax Code of the Russian Federation. However, let us say right away that legislators have not determined new deadlines for 2017. Therefore, the deadlines have not changed. Next, we provide a table with the deadlines for submitting the income tax return in 2017 and remind you on what form to submit the declaration.

Organizations are required to report their profits at the end of the year. The income tax return for the year (tax period) must be submitted no later than March 28 of the year following the reporting year (clause 4 of Article 289 of the Tax Code of the Russian Federation). But this does not mean that you only need to send a declaration to the inspectorate once a year. According to Articles 285 and 289 of the Tax Code of the Russian Federation, all companies must also summarize interim results.

The reporting periods for income tax are the first quarter, half a year and nine months. (Clause 2 of Article 285 of the Tax Code of the Russian Federation).

The declaration for each reporting period must be submitted to the Federal Tax Service no later than the 28th day of the month following this period. The specific deadlines for submitting the declaration depend on how the organization pays advance payments (clause 2 of Article 285, clause 1 of Article 287, clause 3 of Article 289 of the Tax Code of the Russian Federation):

If in 2017 the company makes quarterly advance payments, then the declaration of profit received must be submitted to the Federal Tax Service no later than the 28th day of the month following the end of the quarter (if it falls on a weekend or holiday, the deadline is postponed to the next working day). Below in the table we show the deadlines for submitting the income tax return in 2017 when submitted quarterly.

This new declaration form came into force on December 28, 2016. This means that starting with reporting for 2016, organizations must submit a declaration using a new form. That is, for all the periods of 2017, which you can see in the tables above, you need to use exactly this (new) income tax return form.

The income tax for the 3rd quarter has its own peculiarities in terms of reporting on it. What are they due to? Let's look at this in our material.

The tax period for tax accrued on profits is equal to a calendar year. However, during this period of time, the Tax Code of the Russian Federation (clause 2 of Article 286) requires additional tax calculations to be made to determine the amount of advance payments due on it.

The principle of tax calculation, no matter what period of the year it is calculated for, is the same: the base to which the tax rate is applied is formed on an accrual basis. But the frequency of calculating advances may be different depending on what frequency the taxpayer himself has chosen for them (Clause 2 of Article 285 of the Tax Code of the Russian Federation) - quarterly or monthly.

When calculating monthly, advances are calculated at the end of each month from the profit actually generated for the period from the beginning of the year. In this case, the amount of the advance payment due for payment for the next month is determined as the difference in tax amounts calculated for the current period and the preceding one (clause 2 of Article 286 of the Tax Code of the Russian Federation).

Quarterly calculations are carried out at the end of each quarter of the year using the same approach as for monthly calculations. That is, the base is taken for all quarters from the beginning of the year, and the amount of tax payable for the last quarter is equal to the difference between its values calculated for the current reporting period and the one preceding it.

However, such a simple calculation option is not available to every taxpayer. It can only be used by those whose sales income for the period of time equal to four quarters preceding the quarter of calculation was not higher than 15 million rubles. on average for each of these quarters, as well as budgetary and autonomous institutions, non-profit and foreign organizations, participants in simple and investment partnerships (clause 3 of Article 286 of the Tax Code of the Russian Federation).

Other taxpayers who make quarterly calculations have to complicate the calculation procedure by taking the amount of tax calculated based on the results of work in the next quarter equal to the amount of advances subject to monthly (in the amount of 1/3 of the total amount) payment in the quarter following this period (clause 2 Article 286 of the Tax Code of the Russian Federation). Moreover, due to the fact that the timing of tax calculation based on the results of work for the 4th quarter does not make it possible to focus on its actual values, advances paid in the 1st quarter of the year are considered equal to those established for the last quarter of the previous year, i.e. in the amount actually due for 3 sq. income tax.

Accordingly, at the end of the quarter in which advances calculated according to a complicated algorithm were paid, to determine the amount of tax payable to the budget, it is necessary to take into account not only advances accrued for the previous reporting period, but also their amounts required to be paid for the last quarter of the next reporting period. At the same time, the legislator takes into account that taxable income may decrease, and advances in this case will be paid in excess.

To prepare profit calculations, regardless of whether they are formed monthly or quarterly and how advances are taken into account, the same reporting form is used, approved by order of the Federal Tax Service of Russia dated October 19, 2016 No. ММВ-7-3/572@. This is exactly what you need to focus on when drawing up a profit declaration for the 3rd quarter of 2019.

The frequency of reporting adopted by the taxpayer will be reflected in the special coding of the tax period placed on the title page of the declaration. Despite the fact that the calculation of income tax for the 3rd quarter actually corresponds to its calculation for 9 months and this period is the same for monthly and quarterly reporting, different period codes should be used (Appendix No. 1 to Appendix No. 2 to Order No. MMV-7-3 /572@):

Be sure (in addition to the title page) you will have to fill out sheets reflecting:

Other sections are filled out as necessary, but it is not necessary to include in the profit report for the 3rd quarter sheets intended only for the annual report (Appendix No. 4 to sheet 02, sheets 07, 08, 09, appendices to sheet 09).

Organizations - payers of advances accrued quarterly for the coming months will additionally have to use subsection 1.2 of section 1 and the lines intended to reflect such amounts in sheet 02, and in addition, in lines 210-230 of sheet 02 in the amount of advances attributable to the reporting period, take into account not only the calculated for 6 months tax, but also the amount accrued in the declaration for the half-year in lines 290-310 of advances on profit for the 3rd quarter.

The reflection of monthly advances in the corporate income tax report for the 3rd quarter has one feature, due to which this report differs significantly from other interim reporting. This feature lies in the fact that in this report it is necessary to accrue the amounts of monthly advances paid not only for the next next quarter (fourth), but also for the first quarter of the next year (clause 2 of Article 286 of the Tax Code of the Russian Federation).

To do this, in sheet 02 you need to use not only lines 290-310, usually filled out in the interim report, but also lines 320-340, the name of which directly indicates the inclusion in them of the amounts of advances accrued for the 1st quarter of the next year. Most often, the numbers in sets of lines 290-310 and 320-340 turn out to be the same, and in this case there is no need to generate information in subsection 1.2 of section 1 on two sheets in relation to different quarters (clause 4.3.1 of Appendix No. 2 to Order No. MMV- 7-3/572@). Here it is enough to fill out one sheet, and there is no need to indicate the quarter number.

But if the data on the accrual of advances for the fourth quarter of the current year and the first quarter of the next year turn out to be different (and this is possible in the case of a planned reorganization, closure of separate divisions, entry into a consolidated group), then two sheets of subsection 1.2 of section 1 are filled out and each of them receives their code of the quarter to which the corresponding charges relate (21 - first, 24 - fourth).

It is also possible that the data in subsection 1.2 of section 1 will be completed only for the first quarter of the next year. It arises when a taxpayer, who calculated advances monthly based on actual turnover, wants to switch to quarterly calculations from next year.

When drawing up an income tax return for the third quarter, taxpayers calculating monthly advance payments based on the results of quarterly calculations should remember that this report must show not only advances accrued for the next next quarter of the current year (fourth), but also for the quarter following it (i.e. the first quarter of the next year). To do this, lines 320-340 are additionally used in sheet 02. But subsection 1.2 of section 1 in relation to two different quarters will need to be filled out only in the case when accruals for the fourth and first quarters are made in different amounts. Taxpayers who change the reporting principle from the coming year (from monthly to quarterly with monthly advances) will fill out only one sheet of this subsection (for the first quarter).

Taxation is a dynamically developing process. Changes to the Tax Code of the Russian Federation are made with enviable regularity, and the dates of their entry into force can be different - from one day to several years. Some amendments even come into effect retroactively. Let's look at the most important innovations of 2019 that an accountant will have to take into account in his work.

The object of taxation is, among other things, the gratuitous transfer of goods, work, and services (clause 1, clause 1, article 146 of the Tax Code of the Russian Federation). Consequently, when transferring objects not listed in paragraphs to the state treasury free of charge. 2 p. 2 art. 146 of the Tax Code of the Russian Federation, for example, for socio-cultural purposes, an object of VAT taxation arose. Starting from July 1, 2019, the transfer of social and cultural objects free of charge to the treasury of a republic within the Russian Federation, territory, region, federal city, autonomous region, autonomous district, to the municipal treasury of the corresponding urban, rural settlement or other is excluded from taxation. municipality. The corresponding addition has been made to paragraphs. 2 p. 2 art. 146 of the Tax Code of the Russian Federation.

Thanks to the new paragraph. 19 clause 2 art. 146 of the Tax Code of the Russian Federation, transfer on a gratuitous basis to the state treasury of the Russian Federation is not recognized as an object of taxation not only for movable, but also for immovable property. This eliminates the controversial issue related to the payment of VAT when transferring property to the treasury.

When transferring property free of charge, the transferring party has the obligation to charge VAT, as in a normal sale transaction. At the same time, it is possible to deduct input VAT. However, at the time of gratuitous transfer of real estate, an obligation to restore VAT may arise. The legislator did not forget to make changes here (to clause 10 of Article 171.1 of the Tax Code of the Russian Federation): it is not necessary to restore VAT previously accepted for deduction when transferring real estate to the state treasury (Federal Law dated April 15, 2019 No. 63-FZ).

On July 1, changes regarding the deduction of VAT on the export of works and services came into force (Federal Law No. 63-FZ dated April 15, 2019). Let's look at these changes in comparison with the previous procedure.

From July 1, operations for the sale of works and services are equated to operations subject to VAT, provided that the place of their sale is not recognized as the territory of the Russian Federation and they are not named in Art. 149 of the Tax Code of the Russian Federation. This means that when performing work or providing services, the place of sale of which is not recognized as the territory of the Russian Federation, separate accounting is not required, because in fact, these operations are equated to taxable ones, if they are not named in Art. 149 of the Tax Code of the Russian Federation (Federal Law dated April 15, 2019 No. 63-FZ). Hence the changes in the calculation of the proportion when applying the 5% rule.

According to this rule, all input VAT is deductible if the taxpayer’s share of non-taxable transactions does not exceed 5%. Otherwise, VAT is subject to deduction or is included in the cost according to the proportion. When calculating the proportion, the sale of work or services abroad is equal to taxable transactions, with the exception of those that are exempt under Art. 149 of the Tax Code of the Russian Federation.

VAT on the export of raw materials is deductible on one of the following dates:

VAT when exporting non-commodity goods is accepted for deduction on a general basis, namely, the exporter is a VAT payer, the goods are accepted for accounting, there are the necessary primary documents, as well as a correctly executed invoice. In addition, three years have not yet passed from the date of acceptance of the goods for registration.

Starting from July 1, 2019, the list of raw materials has been reduced. Thus, on a larger number of exported goods, VAT can be deducted without waiting for confirmation of the zero rate. The list of raw materials is given in Decree of the Government of the Russian Federation dated April 18, 2018 No. 466.

In accordance with Federal Law No. 268-FZ dated 08/02/2019, from October 1, 2019, the VAT rate on palm oil becomes 20% instead of 10%, and on fruits and berries - 10% instead of 20%.

From December 1, 2019, paragraphs will be clarified. 12 clause 3 art. 149 of the Tax Code of the Russian Federation (Federal Law dated July 26, 2019 No. 210-FZ). The transfer of goods, works, and services within the framework of charity to organizations and individual entrepreneurs is exempt from VAT. But if previously it was not indicated what documents confirm the right to exemption from VAT, now these documents are spelled out:

It is important that the norm is spelled out in paragraph 3 of Art. 149 K RF, which means that the benefit can be refused.

Federal Law No. 211-FZ dated July 26, 2019 introduces a new paragraph. 36 clause 2 art. 149 of the Tax Code of the Russian Federation, according to which VAT is not assessed on the sale of MSW management services provided by regional operators. Two conditions for the application of the new norm have been established:

At the same time, a duplicate amendment was introduced in paragraphs. 29 clause 3 art. 149 of the Tax Code of the Russian Federation - the sale of utility services is included in VAT-free transactions, subject to their purchase, including from regional operators for the management of solid waste. It is also important here to refer to clause 3 of Art. 149 of the Tax Code of the Russian Federation, which provides the opportunity to refuse benefits.

Income tax

Subsidies received that are not related to the acquisition, creation, reconstruction, modernization, technical re-equipment of depreciable property, acquisition of property rights are included in non-operating income as expenses actually incurred through the subsidy are recognized.

However, the previously unspent portion of the subsidy during three tax periods had to be included in income as of the last reporting date of the third tax period. From January 1, 2018, in clause 4.1 of Art. 271 of the Tax Code of the Russian Federation, changes have been made regarding the timing of the inclusion of subsidies in non-operating income: subsidies are taken into account in income for an unlimited number of years as expenses actually incurred due to these subsidies are recognized (Federal Law dated April 15, 2019 No. 63-FZ).

The norm has been in effect since April 15, 2019, but applies to relations from January 1, 2018, as it improves the situation of taxpayers. For example, if the balance of a subsidy received in 2016 as of December 31, 2018 was taken into account in non-operating income, then the taxpayer has the right to file an amended return for 2018 in order to reduce his tax liability for the year.

Federal Law No. 269-FZ dated August 2, 2019 introduced a new Chapter 1 of the Tax Code of the Russian Federation - Chapter 3.5. Taxpayers are participants in special investment contracts (SPIC). The norm comes into force on January 1, 2020.

The contract will be concluded based on the results of the auction, and the status will be acquired by the person from the moment of entry into the register. The goal of SPIC is the development of modern technologies and production, as well as the establishment of serial industrial production based on them.

For income tax, a new article of the Tax Code of the Russian Federation has been introduced - 284.9 “Features of applying the tax rate to the tax base determined by organizations that have the status of a taxpayer - a participant in a special investment contract.” For SPIC the following are established:

At the same time, amendments were made to the Federal Law of December 31, 2014 No. 488-FZ “On Industrial Policy in the Russian Federation”. Thus, a new chapter 2.1 has been introduced. “Special Investment Contract”, which establishes the subject, parties and content of the SPIC, as well as the procedure for concluding, amending, terminating and terminating the SPIC, monitoring the fulfillment by investors of obligations under special investment contracts and the responsibility of the parties to the special investment contract.

Law No. 210-FZ dated July 26, 2019 expanded the composition of expenses: when transferring social infrastructure objects free of charge, the costs of their creation are included in non-operating expenses on the date of transfer. The norm comes into force on January 1, 2020.

Federal Law No. 210-FZ dated July 26, 2019 lifted the restriction on the application of a zero rate for income tax by educational and medical organizations that was in force until January 1, 2020. Now the zero rate is in effect indefinitely.

In addition, a zero corporate income tax rate has been introduced in relation to:

Temporarily available funds from the capital repair fund placed on a special deposit are not subject to income tax, since from January 1, 2020 they are classified as targeted financing funds that are not taken into account when forming the tax base for income tax.

Previously, the financial department argued that these funds do not fall under the definition of targeted financing and are not recognized as funds of premises owners, therefore they are subject to income tax in the generally established manner (Letters of the Ministry of Finance of the Russian Federation dated 02/22/2017 No. 03-03-06/1/10318, dated 02/08 .2017 No. 03-03-06/3/6643).

Now the rule on what is considered target funds has been clarified in Federal Law No. 137-FZ dated 06/06/2019, having been included in paragraphs. 14 clause 1 art. 251 of the Tax Code of the Russian Federation, new paragraph. Starting from January 1, 2020, targeted financing includes interest accrued for the use of funds in a special account. This means that such income is not subject to income tax. Thus, another legislative gap and controversial issue has been eliminated.

Starting from August 1, 2019, material benefits from interest savings due to the application of mortgage holidays to the borrower are not subject to taxation.

During the grace period, more lenient conditions for repaying a mortgage loan apply to individuals. From the point of view of personal income tax, income may be generated in the form of material benefits from savings on interest. Law No. 158-FZ dated July 3, 2019 established that during this period the taxpayer does not generate taxable income in the form of material benefits.

Federal Law No. 210-FZ dated July 26, 2019 clarified the rules for determining the date of actual receipt of income when writing off a bad debt. From January 1, 2020, a new version of paragraphs is in effect. 5 p. 1 art. 223 of the Tax Code of the Russian Federation - income for interdependent and other persons is determined on the date the debt is recognized as bad.

According to the new clause 62.1 of Art. 217 of the Tax Code of the Russian Federation, taxable income does not arise for individuals if the following conditions are simultaneously met:

Currently, individual entrepreneurs pay advance payments based on the amount of expected income: for half a year, for the third and fourth quarters. At the same time, the tax office calculates the amount of advance payments, and it also breaks it down by payment deadlines. In fact, individual entrepreneurs pay a so-called imputed advance payment.

At the end of the tax period, when filing a declaration in Form 3-NDFL, the personal income tax amount is recalculated by taking into account the advance payments made, and the remaining amount is payable for the previous tax period. In other words, the law forced individual entrepreneurs to “reserve” a certain amount to pay the tax.

From January 1, 2020, the situation will change. Now individual entrepreneurs are forced to keep tax records quarterly, not approximately, but as accurately and correctly as possible, because the amount of advance payments made for personal income tax during the tax period will depend on this.

Individual entrepreneurs' advance payments will now be calculated independently based on the income actually received and applied tax deductions - standard and professional. The corresponding personal income tax rate will be applied to the resulting tax base. Due to the fact that the tax base for personal income tax is determined on an accrual basis for the tax period, the amount of the advance payment payable for a specific quarter will be calculated taking into account the calculated advance payments.

The deadline for paying advance payments also changes: advance payments based on the results of the first quarter, half-year, nine months are paid no later than the 25th day of the first month following the first quarter, half-year, nine months of the tax period, respectively.

Let us remind you that for 2019 advance payments and taxes are paid by individual entrepreneurs no later than:

Merged paragraphs. 1 and 3 tbsp. 217 of the Tax Code of the Russian Federation in paragraph 1 of Art. 217 Tax Code of the Russian Federation. If previously compensation for unused additional days of rest for contract military personnel was not subject to personal income tax, then starting from January 1, 2020, such payments are included in the tax base (Federal Law dated June 17, 2019 No. 147-FZ).

Labor legislation (Article 262 of the Labor Code of the Russian Federation) provides working parents (guardians, trustees) with disabled children with the right to four additional paid days off per month to care for them. You can save up days, for example, for a year, and then you can’t use them. If parents did not use days in the current month, they “burn out” and are not carried over to the next month.

One of the parents (guardian, trustee) can take four days, or they can divide the days between themselves. The employer pays for such days according to average earnings. Despite the fact that such a rule is not directly stated in tax legislation, the highest courts consider such payments as made in accordance with the current legislation, which means they are exempt from taxation (clause 1 of Article 217 of the Tax Code of the Russian Federation, Resolution of the Presidium of the Supreme Arbitration Court of the Russian Federation dated 08.06. 2010 No. 1798/10 in case No. A71-3574/2009-A31).

However, to avoid unjustified disputes in the future, from January 1, 2020, the benefit is enshrined in law in paragraphs. 78 Art. 217 of the Tax Code of the Russian Federation (Federal Law dated June 17, 2019 No. 147-FZ).

By the way, not all accountants know that such payments are not subject to personal income tax.

Let's look at the procedure for providing additional days off:

Tax legislation provides a benefit for birth (adoption, establishment of guardianship). So, if an employer pays one-time financial assistance in connection with the birth of a child, then it is not subject to personal income tax in an amount not exceeding 50 thousand rubles. (clause 8 of article 217 of the Tax Code of the Russian Federation). Such payment is not subject to personal income tax when paying the mother and father of a newborn, even if they work in the same organization (Letter of the Ministry of Finance of Russia dated 07/08/2019 No. 03-04-06/50324).

Financial assistance is paid as a lump sum to parents (adoptive parents, guardians) upon the birth (adoption) of a child during the first year after birth (adoption). Insurance amounts are not calculated. However, if the payment amount exceeds the established limit, then personal income tax and insurance premiums must be paid on the excess amount.

If financial assistance is provided a year after the birth (adoption) of a child, then the entire amount is subject to personal income tax and insurance contributions. And then the contributions can be taken into account in other expenses associated with production and sales (clause 1, clause 1, article 264 of the Tax Code of the Russian Federation, Letter of the Ministry of Finance of Russia dated 02/05/2018 No. 03-03-06/1/6290).

An important caveat is that the payment is made voluntarily by the employer in connection with its social policy or other local acts.

An express course from the Accountant School "" will help you adjust your company's tax policy in 2019 and navigate legal optimization methods. In a short time you will receive structured knowledge and will be able to avoid mistakes in your work.

Organizational property tax

Let's assume the situation. An organization on the territory of one constituent entity of the Russian Federation owns several real estate objects that are registered with different Federal Tax Service Inspectors. In this case, the tax base for each property is determined as the average annual cost. From January 1, 2020, according to the new norm - clause 1.1 of Art. 386 of the Tax Code of the Russian Federation - such a taxpayer has the right to submit a property tax declaration for all real estate objects to one Federal Tax Service Inspectorate of his choice in a notification procedure.

The notification, the form of which is approved by the Federal Tax Service of the Russian Federation, is submitted to the Federal Tax Service on the territory of the constituent entity of the Russian Federation before March 1 of the year of the tax period. The notice must be submitted annually, and during the tax period the taxpayer has no right to change the chosen procedure for submitting the return.

In addition, there is one more important condition under which such a procedure for submitting a declaration is possible: the subject has not established a standard for tax deductions to local budgets. This norm is enshrined in Law No. 63-FZ dated April 15, 2019.

Federal Law dated April 15, 2019 No. 63-FZ, effective January 1, 2020, abolished the obligation to submit calculations for advance payments. However, the advance payments themselves must be paid on time.

The procedure for applying cadastral value changes if it has changed during the tax period. For this, from paragraphs. 1 clause 12 art. 378.2 of the Tax Code of the Russian Federation removed the clarification that the cadastral value is determined as of January 1 of the year, which is the tax period. Thus, if the cadastral value has changed during the tax period, for tax purposes it is taken into account from the date:

Transport tax

You no longer need to pay tax on a stolen car. The Law of April 15, 2019 No. 63-FZ extended this rule to all situations that arose from January 1, 2018. If previously the tax was not paid only on stolen vehicles that were wanted (and if the search was stopped, then the tax had to be paid until it was removed from the register), now the tax is not paid on stolen cars, even if the search is stopped.

The Federal Tax Service will receive information about the “fate” of the stolen vehicle either from documents submitted by the taxpayer or through interdepartmental channels.

There is no need to submit a transport tax return for reporting for 2020. Now the organization’s tax amount will be learned from the Federal Tax Service’s message. The message form was approved by Order of the Federal Tax Service of Russia dated 07/05/2019 No. ММВ-7-21/337@ “On approval of message forms on the amounts of transport tax and land tax calculated by the tax authority, as well as on amendments to the Order of the Federal Tax Service of Russia dated 04/15/2015 No. ММВ -7-2/149@".

The tax office itself will calculate the tax based on the information it has. The message will indicate the object of taxation, the tax base, the tax period, the tax rate, and the amount of calculated tax. The deadline for transmitting the message is within 10 days from the date of its preparation, but no later than 6 months from the end of the tax payment deadline for the previous year. The deadline for paying taxes and advance payments is established by the law of the constituent entity of the Russian Federation.

The new procedure requires the taxpayer to compare the calculation and amount of tax as reported by the Federal Tax Service with his own calculation. If necessary, disagreements must be resolved taking into account the advance payments made. If there is no disagreement, then the tax has been calculated correctly. If the tax was paid in a smaller amount, it must be paid additionally, if in a larger amount, the provisions of Art. 78 Tax Code of the Russian Federation.

If, in the taxpayer’s opinion, the tax office made a mistake in the calculations, it is necessary to submit explanations (documents) within 10 business days from the date of receipt of the message from the Federal Tax Service. The tax office will send its response within a month from the date the inspection received the explanations (documents), if the period for their consideration has not been extended (maximum two months).

If the tax office admits that its calculations are incorrect, it will send the taxpayer an updated message about the calculated amount of tax. If, based on the results of consideration of the taxpayer’s objections, a tax arrears are revealed, the tax office will send a demand for tax payment (clause 1 of Article 70 of the Tax Code of the Russian Federation).

From January 1, 2020, an application procedure for providing documents on the right to benefits will be introduced. For a taxpayer entitled to a benefit, the main thing is to submit an application to the Federal Tax Service. In the absence of supporting documents, the tax office itself will make inquiries to the relevant services.

Land tax

There is no need to submit a land tax return for reporting for 2020 (Federal Law No. 63-FZ dated April 15, 2019).

From January 1, 2020, the mechanism for calculating and paying land tax is similar to transport tax. The tax office will also send a message about the calculated tax amount. Next is a similar procedure for reconciling the calculation. An application procedure for benefits is also being introduced.

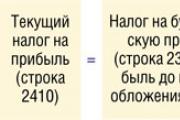

The declaration reflects the financial activities of the organization and shows its profit or loss. It indicates income and expenses incurred. The declaration also reflects the benefits and discounts available to the enterprise, as well as other information. Based on this document, the inspectorate monitors the timeliness of tax payment and its amount.

Tax report can be given in two ways: remotely, through special programs, or personally to the inspection on paper (if the company employs less than 100 people).

The tax rate is 20% . If expenses exceed income, i.e. The organization has no profit and submits a zero declaration.

The declaration is submitted:

The tax is calculated at the end of the tax period - one calendar year. The annual return for the previous year is submittedbeforeMarch 28.

There are also reporting periods, after which advance payments are transferred to the state treasury and reporting is submitted.

This period is considered to be a quarter or, if the organization determines tax based on the profit received, a month. The law establishes that the 28th day of the month following the reporting month is the last day for filing a declaration. If the date falls on a weekend or holiday, the due date is moved forward by the number of holidays or weekends.

The declaration consists of 35 sheets, however, most organizations do not need to complete them all, just 5 pages is enough. The document is being filled out cumulative total. Indicators are taken into account in full rubles. Values less than 50 kopecks are not taken into account, more are rounded.

Always fill out: title page, subsection 1.1., sheet 02 and two appendices to it. Other pages are provided if necessary.

IN title page are filled in:

In the first subsection, line 010 indicates the OKTMO code. Lines 030 and 060 indicate BCC.

The tax rate is 20%, but the money is distributed across two budgets: federal and regional

Lines 040 and 070 indicate the amount of tax that needs to be paid. In this case, advance payments already transferred are taken into account.

For example: the annual profit of the enterprise amounted to 2,160,000 rubles. The declaration for 9 months indicated a profit of 1,550,000 rubles.

Let's calculate the amount of tax to budgets. Profit on which tax was not calculated:

2,160,000 – 1,550,000 = 610,000 rubles.

The following is paid to the federal budget:

610,000 * 2% = 12,200 rub.

The regional budget is paid:

610,000 * 18% = 109,800 rub.

Subsection 2 is intended for companies that make advance payments every month. The quarter is entered in line 001. Further, the payment amounts are specified by month of the quarter and by source of receipt. Lines 120-140 reflect advance payments to the federal treasury, lines 220-240 - to the regional one.

Subsection 3 is required for companies receiving dividends. In line 010 the value 1 is entered. Codes OKTMO and KBK are filled in. In lines 01-21 the dates of tax payment are entered (one day is given after receipt of income), and in the columns opposite - its amount.

Fields 010-040 take into account all income and expenses associated with sales and not.

Fields 010-040 take into account all income and expenses associated with sales and not.

Line 050 is used to reflect losses. Line 060 shows profit (income minus expenses), and field 070 indicates income that can be excluded from it (if any).

Also in this sheet, in lines 080-110, information is filled in, depending on the specifics of the organization’s activities: the availability of benefits, losses that reduce the tax base, non-taxable income. In lines 140-170 the amount of tax rates is filled in. And in lines 180-200 - the amount of tax for the entire period.

Then the advance payment of the previous period is entered (filled out according to the previous declaration) and the amount to be paid is determined. Returning to the example, it turns out that the organization made a profit of 2,160,000 rubles for the year, based on a rate of 20%, the tax for the year will be 432,000 rubles. At the end of 9 months, an advance payment was paid to the budget in the amount of:

1,550,000 * 20% = 310,000 rub.

Accordingly, the following remains to be paid into the budget:

430,000 – 310,000 = 120,000 rubles.

Appendices 1 and 2 to the sheet detail income and expenses. First, in Appendix 1, line 010 indicates the total revenue from sales, then in lines 011-014 it is described in more detail. Finally, non-operating income is filled in. The application for expenses is filled out in the same way.

Appendix 3 is completed for income from the sale of depreciable property, outstanding accounts receivable, land purchased from the beginning of 2007 to the end of 2011, as well as organizations incurring production maintenance costs.

Appendix 4 is completed if there is an untransferred loss. Appendices 5 and 6 are filled out by companies that have separate divisions or are members of consolidated taxpayer groups, respectively.

Used by tax agents shows the calculated tax on dividends. The basis for filling out is the decision of shareholders (if there are several of them, several sections are filled out).

Section A. First, it is necessary to note whether the tax agent is an issuer. Then the type of income is indicated, as well as the period code from the title page. The year for which the payments were made is reflected.

Lines 001 and 010 indicate total dividends (D1). Field 020 shows income paid to Russian companies. Fields 021-024 detail the previous tax rate indicator. If there are other sources of payments, individuals and foreign companies must fill in fields 030-070.

Line 081 reflects the income from which tax is calculated (D2). In line 080, income that is not taken into account for taxation (0% rate) is added to it. To fill in lines090, 091 and 092use formulas:

D1 - D2 = 090

023 / 001 * 090 = 091

021 / 001 * 090 = 092

Line 091 * 13% = line 100

Lines 110 and 120 indicate the amounts of dividends already paid in previous or current periods, respectively.

Section B is a detail to section A and is filled out for each source of payment. Field 060 is the amount of income, field 070 is the tax on it.

Section B reflects the amount of income and the calculated tax on it for government securities.

Intended for companies that receive income in the form of dividends on government or private securities. They are taxed at rates of 15%, 13%, 9% and 0%. Select the required code in the appropriate field. If there is income from different types of securities, fill in several sheets.

Line 010 shows the total amount of income. Line 020 indicates income that can reduce the tax base. The tax rate (030) is determined by the type of dividends. Line 040 – tax amount.

Fields 050 and 060 are used if there is income from shares in foreign companies (“Type of income” - 4); amounts paid outside the Russian Federation in previous and current reporting periods are reflected here.

Line 070 shows the amount of tax for previous reporting periods, line 080 - for the current quarter.

If the company has transactions with securities that are accounted for in a special manner, sheet 05 is filled out. A code is selected that reflects the essence of the transaction. Codes “1” and “2” are not used by professional market participants.

If the company has transactions with securities that are accounted for in a special manner, sheet 05 is filled out. A code is selected that reflects the essence of the transaction. Codes “1” and “2” are not used by professional market participants.

Field 010 – the amount of income from disposal, broken down by lines 011-014. Field 020 - expenses with details on lines 021-024. They are accounted for at the cost of acquiring the security. Field 040 - profit. The profit adjustment is carried out on line 050. The final result is reflected in line 060.

If an organization has a loss that can reduce the tax base, it is entered in field 080. In line 100, the tax base is adjusted taking into account this indicator.

Fill in only NPF. Field 010 shows their total income. Fields 020-110 specify them by individual types.

Line 120 indicates the amount of pension reserves placed by NPFs. This amount also includes the balance of insurance reserves available to the organization at the beginning of 2002.

Line 130 (the sum of lines 140-180) shows the amount of profit received from interest on the placement of funds and securities, taken into account based on the Central Bank refinancing rate.

When calculating, other expenses are excluded from lines 200 and 220. Line 190 reflects expenses incurred in connection with the placement of reserves.

Lines 200 and 210 take into account expenses incurred during the sale or disposal of securities traded or not traded on the Securities Market, respectively. Line 220 reflects expenses incurred in the implementation of other projects.

Line 230 of the NPF indicates the percentage of deductions from income that it uses for statutory activities. Lines 240, 241 and 242 reflect the amounts of deductions for the formation of property (the sum of lines 250-320).

The profit received by the fund from operations with securities is shown on line 330 (traded on the securities market) or on line 350 (non-traded on the securities market). Income from other investments is reported on line 390.

Fields 340, 360 and 400 reflect the amounts that can be excluded from profit. If there is a loss in lines 330, 350, 390, the tax base is recognized as equal to “0”.

Profit received from the placement of government (municipal) securities is indicated in lines 370 and 380.

Then the tax bases are calculated separately by type of profit, these are lines 410, 450 and 490. Line 530 indicates the final result for calculating the tax.

Lines 460-480 and 500-520 reflect the amounts of losses for the past, current and future periods, respectively.

Designedfor non-profit charitable organizationstions. They report on the intended use of allocated funds. Government subsidies and budgetary allocations are not taken into account.

Designedfor non-profit charitable organizationstions. They report on the intended use of allocated funds. Government subsidies and budgetary allocations are not taken into account.

Column 1 contains the codes of the funds received. The date of receipt of funds and the period of use are reflected in columns 2-5. Receipts from previous periods that were not fully used are taken into account.

The amount of property, funds, period of use that has not expired is indicated in columns 3-6.

Column 4 shows the amount of funds used for their intended purpose. If there are funds used for other purposes or not used at all, column 7 is filled in. They are included in non-operating income.

To be filled inwhen an enterprise has interdependentcounterparties,and transaction pricessamemarket. To avoid understated profits and tax audits, the company can independently adjust the tax base.

The section also allows you to display symmetrical (as income increases, expenses increase) and reverse adjustments. A separate sheet is filled out for each correction, even if there is only one counterparty.

When filled out, the corresponding adjustment code is reflected. If we are talking about independent or symmetrical adjustments, it is necessary to attach an explanatory note that will allow the transaction to be identified.

Lines 010-040 indicate the amount of the adjustment. Lines 010 and 020 are income from sales and non-operating income, respectively. Lines 030-040 – expenses. If the adjustment leads to an increase in the indicator, 1 is put in the “Characteristic” column, if it leads to a decrease - 0. Line 050 is the total, the sum of the four previous lines.

Line 050 indicates the calculated adjustment value, calculated as the sum of the numerical values of completed lines 010-040 (modulo).

Lines 060 and 070 reflect income and expenses from disposal (for transactions with securities). The sign is affixed in the same way. Line 080 summarizes the total (060 + 070).

In chapterAThis sheet fills in information about the controlled foreignorganizations:

Section B1 is intended for companies falling under paragraphs. 1 clause 1 art. 309.1. Tax Code of the Russian Federation. The number of the controlled company is entered, identical to sheet A. Then the digital currency code is indicated (according to financial statements).

Line 010 shows total profit before taxes. Line 020 reflects the amount of adjustment to this profit. Lines 021-023 show the amount of dividends that go towards reducing profits. Lines 024-032 reflect income and expenses that do not affect the tax base.

Line 040 (adjusted profit) = line 010 – line 020

Field 050 shows the loss, field 060 shows the tax base (040 – 050). If the result is a negative value, “0” is entered in the declaration. Indicators in lines 010-060 are filled in in currency.

Line 070 displays the value of the tax base in terms of Russian currency. The tax amount is indicated in line 090.

Section B2 is intended for companies falling under paragraphs. 2 p. 1 art. 309.1. Tax Code of the Russian Federation. Fill in the same way.

Such a declaration is submitted in a simplified form on sheet 02; in its appendices only the TIN and KPP of the organization, the tax rate and page number are filled in. The remaining columns are marked with dashes. If the organization had income and expenses, but no net profit, the declaration is filled out in the usual manner and “zero” is called only conditionally.

Failure to submit or late submission of a declaration is punishable by administrative responsibility. By decision of the court, a fine may be imposed on an official from 300 to 500 rubles. The organization is subject to fine 5% from the tax amountfor all months of delay(even for less than a month).

The fine imposed cannot be less than 1000 rubles. The upper limit is 30% of the tax amount. If the delay exceeds 180 days, an additional penalty of 10% of the tax amount is charged for each subsequent month. Accounting is carried out in working days.

It is possible to hold an organization accountable even if the deadlines are missed by one day and even if a “zero” declaration is submitted.

You can learn more about the filling features from the video:

An example of a correct income tax return in 2017, download a new current form for free in Excel. What...

P. S. Pallas (1741 - 1811) - naturalist and traveler-encyclopedist, who glorified his name with major contributions to...

Today, all issues related to the placement of government orders are regulated by the Law on the Contract System -...

Accounting Regulations Accounting for calculations of income tax of organizations PBU 18/02 (as amended by Orders of the Ministry of Finance of the Russian Federation...

A trainee salesperson is usually called those salespeople who are not yet ready to work completely independently. Process...

Educational institution "Gomel State Medical University" Department of Neurology and Neurosurgery...

One of the most controversial and controversial methods for the early development of children was developed in the 80s by a sociologist...

Contents Dietary supplement based on an extract obtained from the fly beetle (or...

Ekaterina MirimanovaSystem minus 60. RevolutionSystem minus 60 with Ekaterina Mirimanova“System minus 60....

Heaviness and bloating are the causes of both ordinary overeating and more serious digestive problems...

The second blood group, Rh-negative, appeared many years ago, when a person ceased to be...

PSYCHOLOGICAL ASPECTS OF ANOREXIA PHENOMENON (EXPERIMENTAL STUDY) T. V. Tarasova, E. V. Arsentieva...

Contents Since the skin in this area is thin, it is more prone to the appearance of various types of spots....

vseslav Sat, 10/17/2015 - 20:50 Vasileostrovskaya station is one of the oldest stations...

P. S. Pallas (1741 - 1811) - naturalist and traveler-encyclopedist, who glorified his name with major contributions...

Today, all issues related to the placement of government orders are regulated by the Law on Contract...